Glass-Steagall Repeal: The 9 Who Voted Yes Still Run the Senate

Of 100 senators who repealed Glass-Steagall in 1999, nine still serve in 2026. All nine voted yes. They now run Finance, Appropriations, and the Senate floor.

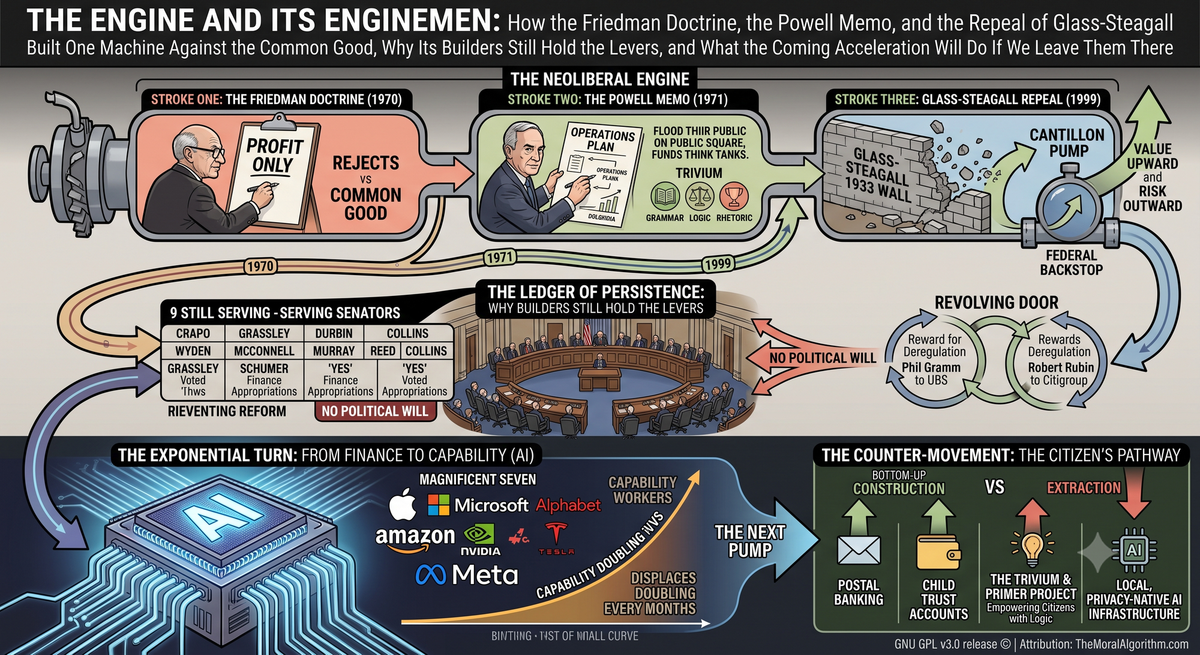

How the Friedman Doctrine, the Powell Memo, and the Repeal of Glass-Steagall Built One Machine Against the Common Good, Why Its Builders Still Hold the Levers, and What the Coming Acceleration Will Do If We Leave Them There

A working paper of TheMoralAlgorithm.com

Thesis

The neoliberal turn is not three separate events that happened to point the same way. It is one engine with three strokes. Milton Friedman wrote the doctrine that made private profit the only duty a firm owes. Lewis Powell wrote the field manual for turning that doctrine into control of courts, campuses, and the Congress. The repeal of Glass-Steagall was the doctrine and the manual cashed out in law, the moment the theory became plumbing. Run the three through the tests the Moral Algorithm was built to run, the Veil of Ignorance, the Aristotelian mean, and the systemic reading of who stands nearest the money, and each one fails the same way, for the same reason: each optimizes for the holder of capital and treats the common good as an externality to be priced, ignored, or captured.

This paper does three things. It validates that reading against the record. It names the people who built the machine and shows, with the roll call in hand, that they did not retire into history; they rose to run the very committees that would have to dismantle it. And it projects the engine forward into the near future, where artificial intelligence is about to hand the same owners a lever with far more torque than finance ever gave them. The argument ends where honesty requires: with the counter-movement, the bottom-up build of capital and civic competence that the Citizen's Pathway proposes in place of top-down extraction.

Part One. One Engine, Three Strokes

Stroke one: Friedman, 1970. The doctrine.

On September 13, 1970, the New York Times Magazine ran Milton Friedman's essay "The Social Responsibility of Business Is to Increase Its Profits." The title is the argument. Friedman held that a corporate executive is an employee of the shareholders, that the only social responsibility of business is to raise profit inside the rules of the game, and that any manager who spends shareholder money on the broader community is taxing owners without their consent. He called the language of social responsibility a form of collectivism and treated the common good as a category error when applied to a firm.

Set this beside the Moral Algorithm and the clash is total, not partial. The Algorithm grounds civic ethics in John Adams, John Rawls, and Aristotle, and it holds the common good as the thing policy is for. Friedman holds the pursuit of private interest as the highest business duty and rejects any claim the community has on the firm. These are not two dialects of one economics. They are inverses.

Run Friedman through the Veil of Ignorance. Rawls asks you to design the rules before you know your station, your class, your luck. Behind that veil, no rational person designs a society tuned only for the owners of capital, because the odds you are born an owner are small and the cost of being born anything else is steep. The Friedman Doctrine only looks rational to a chooser who already knows he will be a shareholder. Strip that knowledge away and no one picks it. A rule that only a lucky insider would choose is, by Rawls's own test, unjust. Friedman's doctrine fails at the door.

Run it through Aristotle. Virtue lives at the mean, and the healthy city balances the flourishing of the many against the ambition of the few. A doctrine that elevates one appetite, the appetite for private gain, to the status of sole duty is the textbook Aristotelian vice: excess. It is not liberty. It is license dressed as principle.

Stroke two: Powell, 1971. The field manual.

Eleven months later, on August 23, 1971, corporate lawyer Lewis F. Powell Jr. sent a confidential memorandum to the U.S. Chamber of Commerce titled "Attack on the American Free Enterprise System." The Powell Memo is not a philosophy. It is an operations plan. It urged business to stop reacting and start building: to fund scholars and place them, to shape textbooks and campus speech, to staff the think tanks, to litigate as a long game, and above all to treat the courts as, in Powell's own reading, the most important instrument of social and economic change available to the patient and the well-funded. Two months after he wrote it, Richard Nixon nominated Powell to the Supreme Court. The Senate confirmed him in December 1971. The man who wrote the manual for capturing the courts took a seat on the highest one.

Set this beside Ordered Liberty and the clash is structural. A republic that governs itself needs three things the memo is designed to corrode: civic competence in ordinary citizens, an honest public square, and reasoning that can be checked. The Trivium names the mechanism. Grammar is the ground of shared fact, the retrieved and agreed-upon record. Logic is the discipline of valid inference. Rhetoric is honest persuasion. The Powell plan pays to poison each layer at the source. It funds institutions whose product is not the true thing but the useful thing, a stream of confident, well-produced, pre-decided conclusions that arrive wearing the costume of scholarship. It does not win the argument. It floods the channel so the argument cannot be had.

That is the deeper harm, and it is worth stating plainly. Friedman corrupts the goal by making private gain the only end. Powell corrupts the process by making public reason for sale. A citizen can survive a bad argument. A citizen cannot reason at all inside a public square where the grammar itself has been bought.

Stroke three: Glass-Steagall repealed, 1999. The plumbing.

The Banking Act of 1933, the Glass-Steagall Act, drew a hard line after the Crash: commercial banking, where deposits carry a federal guarantee, would be kept apart from investment banking, where the house bets for its own account. The wall stood for the longest crisis-free stretch in the history of American finance. In 1998 Citicorp and Travelers merged to form Citigroup, a combination that was illegal on its face under Glass-Steagall and the Bank Holding Company Act. The Federal Reserve granted a temporary waiver in September 1998 on the working assumption that the law would soon be changed to fit the merger, rather than the merger unwound to fit the law.

It was. On November 4, 1999, the conference report of the Gramm-Leach-Bliley Act passed the Senate 90 to 8 and the House 362 to 57. President Clinton signed it on November 12. The wall came down, and the Citigroup that had already been built in defiance of the old law became legal after the fact. Eight senators voted no. Their names deserve the record: Boxer, Bryan, Dorgan, Feingold, Harkin, Mikulski, Shelby, and the late Paul Wellstone.

Read this through the Cantillon Effect and the machinery is exposed. Richard Cantillon saw it three centuries ago: new money does not enter an economy evenly. It enters at a point, and whoever stands nearest that point spends it first, at old prices, before the new money has bid prices up. Those far from the spigot get the money last, after it has already lost value, and they carry the inflation the early spenders escaped. Merging insured deposit banking with speculative trading built a new spigot and set the financial sector's own hand on the valve. Credit and leverage generated through speculative vehicles flowed first to the people closest to their creation. The public carried the risk through deposit insurance and, when the bets went bad, through the bailout. The gains privatized upward. The losses socialized outward. That is not a market outcome. That is a Cantillon pump with a federal backstop welded to the intake.

A fair thesis states the strongest objection to its own case. Some serious economists, Bill Clinton among the defenders, along with Brad DeLong and Tyler Cowen, argue that the repeal did not cause the 2008 crisis and may have softened it, since the firms that failed hardest, Lehman and Bear, were the least diversified, and the diversified banks weathered it better. Grant the narrow point and the argument still holds, because the charge here is not that one statute single-handedly caused one crash. The charge is directional. The repeal hyper-consolidated the banking system, welded the public guarantee to private speculation, and moved the whole structure toward concentration and away from the common good. On that, the concentration that followed is not in dispute. It is measurable, and it kept climbing.

Part Two. The Timeline of the Engine

| Year | Event | What it installed |

|---|---|---|

| 1933 | Glass-Steagall Act | The wall between insured deposits and speculation |

| 1970 | Friedman, "The Social Responsibility of Business Is to Increase Its Profits" | The doctrine: private profit as sole corporate duty |

| 1971 | Powell Memo to the U.S. Chamber of Commerce (Aug 23) | The manual: capture courts, campuses, and think tanks |

| 1971 | Powell nominated to the Supreme Court (Oct), confirmed (Dec) | The manual's author on the highest bench |

| 1987 | First Financial Services Act versions introduced by Gramm and Leach | The first push to breach the 1933 wall |

| 1998 | Citicorp-Travelers merger; Fed grants temporary waiver | The illegal combination, built on a bet the law would bend |

| 1999 | Gramm-Leach-Bliley signed (Nov 12) | The wall removed; the merger legalized after the fact |

| 2000 | Commodity Futures Modernization Act | Derivatives, including credit default swaps, left unregulated |

| 2008 | Global financial crisis; Citigroup bailed out | The pump's first public reckoning |

| 2023-2026 | AI capital concentration; the Magnificent Seven pass one-third of the S&P 500 | The same engine, re-tooled for a new source of rents |

The strokes are decades apart. The direction never changes.

Part Three. The Ledger of Persistence

Here is the part that turns a history lesson into a live problem. The people who cast the defining vote did not fade out. They moved up.

Of the one hundred senators who sat in the chamber for the November 4, 1999 vote to repeal Glass-Steagall, nine still hold their seats in 2026. That is nine percent of that chamber, still in office more than a quarter century later. Every one of the nine voted yes. Not most. Not a majority. All nine. Of the eight senators who voted no, not one remains. The dissent left. The engineers stayed.

And they did not stay as backbenchers. Look at where the nine sit now, in the 119th Congress.

| Senator (1999 vote: Yea) | Seat since | Position held in 2026 |

|---|---|---|

| Chuck Grassley (R-IA) | 1981 | President pro tempore of the Senate; third in the line of succession |

| Mitch McConnell (R-KY) | 1985 | Longest-serving Senate party leader in U.S. history |

| Chuck Schumer (D-NY) | 1999 | Senate Democratic Leader |

| Dick Durbin (D-IL) | 1997 | Senate Democratic Whip; ranking member, Judiciary |

| Patty Murray (D-WA) | 1993 | Vice chair / ranking member, Appropriations |

| Ron Wyden (D-OR) | 1996 | Ranking member, Finance |

| Jack Reed (D-RI) | 1997 | Ranking member, Armed Services |

| Susan Collins (R-ME) | 1997 | Chair, Appropriations |

| Mike Crapo (R-ID) | 1999 | Chair, Finance; Chief Deputy Republican Whip; former chair, Banking |

Read that table slowly, because the pattern in it is the whole argument about political will. The Senate Finance Committee oversees more than half the federal budget and holds jurisdiction over tax and the financial architecture. Its chairman, Mike Crapo, voted to repeal Glass-Steagall. Its ranking member, Ron Wyden, voted to repeal Glass-Steagall. The chair and the ranking member of the committee that would have to lead any financial re-regulation both cast the same yes. The Appropriations Committee is the same story: chair Collins and ranking member Murray, both yes. The President pro tempore, Grassley, third in line to the presidency, voted yes. Both party whip offices are held by yes votes. The Democratic Leader voted yes.

This is why there is no political will, and the honest explanation is not a conspiracy. It needs no secret meeting and no back-room signal. It is simpler and harder to fix than a plot. Reform would require these specific individuals to repudiate the defining vote of their own long careers, at the exact committees where they now hold the gavel or the ranking chair. The incentive gradient runs one way, and it has run one way for twenty-seven years. You do not need to whisper to a machine whose operators were promoted for building it.

Both chambers: the persistence runs all the way to the top of Congress

The Senate roll call gives the cleanest single statistic, but the pattern does not stop at the Senate door. The repeal cleared the whole Congress on the same day, the House 362 to 57 and the Senate 90 to 8, and the House side carries the argument even higher, because it reaches the people who run the building today.

Count both chambers and roughly three dozen sitting members of the 2026 Congress cast a vote on the 1999 repeal. Some were in the House then and remain in the House now. Others crossed the rotunda. John Thune voted yes as a House member in 1999 and now serves as Senate Majority Leader. Lindsey Graham, Jerry Moran, and Roger Wicker, the chairman of Armed Services, all voted yes in the House and all now sit in the Senate. Add the nine Senate survivors and the picture sharpens to a single fact that no partisan can wave away: the two people who run the United States Senate in 2026, Majority Leader John Thune and Democratic Leader Chuck Schumer, both voted to repeal Glass-Steagall. So did the President pro tempore, Chuck Grassley, third in the line of succession. The floor is run, on both sides of the aisle, by yes votes.

Here is the House side laid out the same way, every member who voted on roll call 570 in 1999 and still sits in Congress in the 119th. Those listed as "now in the Senate" carried their yes or no across the rotunda.

| Representative (1999) | 1999 vote | Where they sit in 2026 |

|---|---|---|

| John Thune (SD) | Yea | U.S. Senate; Senate Majority Leader |

| Roger Wicker (MS) | Yea | U.S. Senate; chair, Armed Services |

| Lindsey Graham (SC) | Yea | U.S. Senate |

| Jerry Moran (KS) | Yea | U.S. Senate |

| Ed Markey (MA) | Nay | U.S. Senate |

| Bernie Sanders (VT) | Nay | U.S. Senate |

| Nancy Pelosi (CA) | Yea | U.S. House; former Speaker |

| Steny Hoyer (MD) | Yea | U.S. House; former Majority Leader |

| James Clyburn (SC) | Yea | U.S. House; former Democratic whip |

| Richard Neal (MA) | Yea | U.S. House; former chair, Ways and Means |

| Frank Pallone (NJ) | Yea | U.S. House; top Democrat, Energy and Commerce |

| Jerrold Nadler (NY) | Yea | U.S. House; former chair, Judiciary |

| Bobby Scott (VA) | Yea | U.S. House; top Democrat, Education and Workforce |

| Zoe Lofgren (CA) | Yea | U.S. House |

| Bennie Thompson (MS) | Yea | U.S. House; former chair, Homeland Security |

| Sanford Bishop (GA) | Yea | U.S. House |

| Lloyd Doggett (TX) | Yea | U.S. House |

| Diana DeGette (CO) | Yea | U.S. House |

| Hal Rogers (KY) | Yea | U.S. House; former chair, Appropriations |

| Robert Aderholt (AL) | Yea | U.S. House |

| Chris Smith (NJ) | Yea | U.S. House |

| Mike Simpson (ID) | Yea | U.S. House |

| Marcy Kaptur (OH) | Nay | U.S. House |

| Rosa DeLauro (CT) | Nay | U.S. House; top Democrat, Appropriations |

| Maxine Waters (CA) | Nay | U.S. House; top Democrat, Financial Services |

| John Larson (CT) | Not Voting | U.S. House |

The table is a floor, not a census. Retirements and midterm changes can move it by a seat or two, and a few names may have stepped down since the 119th Congress convened. Read it as the shape of the thing, not a certified count. The shape is the point: the yes votes did not just survive, they took the leadership, the Majority Leader's chair in the Senate and the former Speaker's gavel in the House among them, while the House dissent that remains sits mostly as ranking members and back-benchers.

Honesty requires the other half of the House picture, because it is where the two chambers differ. In the Senate, every 1999 survivor voted yes, without exception. In the House, several long-serving members who still hold their seats voted no, among them Marcy Kaptur of Ohio, Rosa DeLauro of Connecticut, and Maxine Waters of California. The House dissent did not all leave the way the Senate dissent did. That nuance does not soften the thesis; it tightens it. The claim was never that every veteran of that Congress is complicit. The claim is that the people promoted to run Congress are the people who voted for the machine, and the leadership roster proves it. Dissenters can survive on the backbench. The gavels went to the builders.

The lobbyists: the revolving door as reward structure

The persistence is not only in office. It ran through the door that connects office to the industry it was meant to police, and the door paid well.

A clean percentage cannot be put on the lobbying side the way it can on the roll call, because the lobbying apparatus is institutional and self-replacing rather than a fixed roster of countable people. The think tanks Powell called for still run. The U.S. Chamber of Commerce still lobbies. The revolving door still turns. What can be shown, by name, is the reward structure that keeps the door turning, and the cases are not obscure.

Phil Gramm, the Senate sponsor whose name sits first on the act, retired from the Senate in 2002 and joined UBS as a vice chairman of its investment bank the same year, a role a fellow observer described as adviser and lobbyist rather than operator. He held it until 2012. He wrote the wall down, then took a chair on the far side of it. Robert Rubin, the Treasury Secretary who drove the repeal from inside the Clinton administration, stepped down and resurfaced as a senior figure at Citigroup, the very conglomerate the repeal legalized, for compensation reported near one hundred and twenty million dollars over his tenure. When Citigroup collapsed in 2008 it took roughly forty-five billion dollars in direct federal rescue and hundreds of billions more in guarantees. Rubin left with his pay. Lawrence Summers, who championed the repeal and called it legislation that would let American firms compete in the new economy, succeeded Rubin as Treasury Secretary and later ran the National Economic Council. Sandy Weill and John Reed of Citigroup led the lobbying that pushed the bill over the line. Reed, years later, called the repeal a mistake. The confession came after the payday.

The lesson is not that individuals were wicked. The lesson is that the system paid, richly and reliably, for exactly the votes and the advocacy that served capital, and paid nothing for dissent. When the reward for building the pump is a seat at the top of the firm the pump enriched, you do not need to explain the lack of reform. You have already explained it.

Part Four. The Logic of No Reform

Put the two persistences together, the roster and the door, and the absence of political will stops being a mystery and becomes an equation.

The people with the power to re-regulate are the people who deregulated. The reward for deregulating was promotion inside government and wealth outside it. The penalty for dissent was a short career. The public square that might have forced a reckoning is the same square the Powell manual was written to flood, and the flooding worked; the think tanks that manufacture the pro-concentration case are older, richer, and more numerous now than in 1971. So the machine faces no serious internal pressure to reverse, and the external pressure has been engineered down at the source. This is a closed loop, and it was designed to close.

That is the honest, structural account, and it is more damning than any cabal, because a cabal can be exposed and broken. A structure that rewards its own builders and starves its own critics does not need to hide. It only needs to keep paying.

Part Five. The Exponential Turn

Now project the engine forward, because the near future is where this stops being history and becomes the decisive fight of the age.

Everything above describes a machine that concentrates the gains of a new money source in the hands of whoever stands nearest its creation, while spreading the risk and the cost to everyone else. Finance was one such source. Artificial intelligence is the next one, and it is a far more powerful pump, because it concentrates not just capital but capability itself.

Consider the capability curve first, because it is the part most people underrate. The research group METR measures how long a task an AI agent can complete on its own before it fails. Across six years the length of task a frontier model can finish at even odds has doubled roughly every seven months, and on the recent trend the doubling has tightened toward four months. In plain numbers, an agent went from handling work that took a human about nine seconds in 2020 to work that took a human about fourteen and a half hours by February 2026, nearly four orders of magnitude in six years. At the current rate the same researchers project week-long autonomous tasks by late 2026 and month-long tasks by the middle of 2027. That is not a forecast of a distant marvel. That is next year.

Now consider who owns the pump. As of mid-2026 seven companies, Apple, Microsoft, Alphabet, Amazon, Nvidia, Meta, and Tesla, make up roughly a third of the entire S&P 500, with a combined market value above twenty-two trillion dollars. In 2015 those same firms were about an eighth of the index. Nvidia alone rose on the order of eight hundred percent from the start of 2023 and now accounts for more than a fifth of the group by itself. In 2025 AI-linked names drove the majority of the market's gain; strip technology out and the index barely moved. Reported hyperscaler capital spending for the AI build-out runs to the hundreds of billions of dollars a year. And by one reckoning drawn from Oxfam's early-2026 figures, billionaire wealth jumped sixteen percent in 2025 to more than eighteen trillion dollars, roughly three times the recent pace.

This is the Cantillon Effect again, at a scale finance never reached, because the new resource is not just money but the machine that does the work. When capability itself concentrates in seven firms, the people nearest that creation capture the value first, and everyone else meets it as displacement. The early labor signals are already visible in the reporting. In 2025, outplacement trackers attributed tens of thousands of U.S. job cuts directly to AI, inside a total of more than a million cuts that ran well above the prior year. In March 2026 one payments firm cut its workforce from roughly ten thousand to under six thousand and named automation as the reason. The gains flow up to the owners of the model. The costs land on the worker whose task just crossed the capability line.

Run this through the same three tests and the verdict is identical to Friedman's, only sharper. Behind the Veil of Ignorance, no one designs a world where the fruit of a general-purpose technology accrues to seven companies while the displaced carry the loss, unless the chooser already knows he owns the shares. By the Aristotelian mean, capability concentrated this hard, this fast, with no counter-weight, is excess of the most dangerous kind. And structurally, the same class that captured finance is capturing compute, with the same doctrine (Friedman's), the same captured public square (Powell's), and now a pump with an engine block instead of a spigot.

Here is the hinge of the whole paper. The neoliberal engine took thirty years to move the country from the 1970 doctrine to the 1999 repeal to the 2008 reckoning. The AI turn is compressing that arc from decades into quarters. The task-horizon doubling is measured in months. The market concentration is measured in single years. If it took a generation to build the financial pump and we still cannot re-regulate it because its builders run the committees, ask the obvious question about a pump that is being built in quarters by an even smaller circle of owners. The window to shape it is not opening. It is closing, and it is closing on the exponential's schedule, not on the legislative one.

Part Six. The Counter-Movement

Diagnosis without a build is just despair with footnotes. The Citizen's Pathway answers extraction with construction, and it answers top-down with bottom-up, because the flaw in the engine is not that it moves money; it is the direction it moves it.

Where Glass-Steagall's repeal welded the public guarantee to private speculation and pumped value upward, the American Capital and Competence Act runs the pump the other way. Postal banking puts a public, non-speculative banking option at the counter every community already has, breaking the private choke-point on basic financial access. Child trust accounts seed capital at the bottom of the ladder, at birth, so that ownership is not an inheritance reserved for people who already stand near the spigot. These are not charity. They are structural counter-Cantillon devices: they move the point where new value enters the economy away from the financial sector's own hand and toward the citizen.

Where the Powell manual bought the grammar of the public square, the Trivium and the Primer Project give it back, by equipping ordinary citizens to hold the grammar of shared fact, run the logic of an argument, and see through the rhetoric that was manufactured to move them. A citizen who can run the Trivium on a think-tank talking point is a citizen the Powell strategy cannot flood. Civic competence is not a soft complement to structural reform. It is the precondition for it, because a captured public square will never demand the reform in the first place.

And where the AI turn threatens to concentrate capability itself, the same principle scales up: capability, like capital, has to be built from the bottom or it will be owned from the top. Local and privacy-native infrastructure, public and cooperative access to compute, and civic literacy about how these systems actually work are the capability-era versions of postal banking and the child trust account. The choice is the same choice the country faced in 1933 and lost in 1999. Concentrate the new power in the hands nearest its creation, or distribute it so the many can hold it. We know what the first road looks like, because we have driven it for fifty years and the drivers are still at the wheel.

Verdict

The Friedman Doctrine, the Powell Memo, and the repeal of Glass-Steagall are not a neutral economic theory that history happened to sour on. They are a deliberate machine, tuned to optimize for private interest and to treat the common good as an externality. Run through the Veil of Ignorance, the Aristotelian mean, and the Cantillon reading, all three fail the same test the same way. The builders of that machine were not punished. They were promoted, and nine of them still hold the levers, every one a yes vote, sitting today atop Finance, Appropriations, the whip offices, and the President pro tempore's chair. That is the whole reason the will to reform never comes: you cannot ask a machine to dismantle itself when its operators were promoted for building it.

And now the same owners are picking up a bigger lever. The financial pump took thirty years to build and we still cannot turn it off. The AI pump is being built in quarters. If the Moral Algorithm means anything, it means this: the warnings are not ahead of us waiting to be read. They are behind us, signed into law, holding the gavels, and the only question left is whether we build the counter-movement before the next stroke of the engine fires, or after.

The engineers already know the answer they prefer. They wrote it down in 1970, mailed it in 1971, and passed it in 1999. The rest of us have not answered yet.

Publishing metadata (for Ghost SEO fields)

- Display title (H1): Congress Repealed Glass-Steagall in 1999. The Men Who Voted Yes Now Run Both Chambers.

- SEO meta title (~59 characters): Glass-Steagall Repeal: 1999's Voters Still Run Congress

- Meta description (149 characters): Congress repealed Glass-Steagall in 1999, 90-8 and 362-57. Today the Senate's Majority Leader, Minority Leader, and President pro tempore all voted yes.

- Note: The nine-of-nine "all voted yes" claim holds cleanly for the Senate survivors and for current Senate leadership. It does not hold for the whole House, where some still-serving members (Kaptur, DeLauro, Waters) voted no. Keep public-facing claims at the leadership level to stay accurate.

Released under the GNU General Public License v3.0. Attribution: TheMoralAlgorithm.com.

Sources and notes

- Gramm-Leach-Bliley Act conference report votes, November 4, 1999: Senate 90-8, House 362-57. U.S. Senate roll call vote 354, 106th Congress, 1st session; Congress.gov actions for S.900.

- Full Senate roll call and the eight dissenting votes (Boxer, Bryan, Dorgan, Feingold, Harkin, Mikulski, Shelby, Wellstone): U.S. Senate roll call vote 106-1-354.

- The nine 1999 senators still serving in the 119th Congress and their present positions: cross-referenced from the 1999 roll call against current Senate leadership and committee rosters (Grassley as President pro tempore per S.Res.3, 119th Congress; Crapo as Finance chair; Collins as Appropriations chair; Wyden, Murray, Reed, Durbin as ranking members; Schumer as Democratic Leader; McConnell in office).

- House conference-report vote, roll call 570, November 4, 1999, 362-57: Office of the Clerk of the U.S. House. Cross-referenced against the 2026 (119th Congress) membership. Current members who voted yes in the 1999 House include John Thune (now Senate Majority Leader), Lindsey Graham, Jerry Moran, and Roger Wicker (now senators), alongside long-serving House members. Current members who voted no in the 1999 House and still serve include Marcy Kaptur, Rosa DeLauro, and Maxine Waters. The combined both-chambers count of sitting 2026 members who voted on the repeal is roughly three dozen; treat it as a floor, since individual retirement dates can shift it by one or two.

- Friedman, "The Social Responsibility of Business Is to Increase Its Profits," New York Times Magazine, September 13, 1970.

- Lewis F. Powell Jr., "Attack on the American Free Enterprise System," memorandum to the U.S. Chamber of Commerce, August 23, 1971; nominated to the Supreme Court October 1971, confirmed December 1971.

- Citicorp-Travelers merger (1998) and the Federal Reserve's temporary waiver (September 1998).

- Revolving-door cases: Phil Gramm to UBS (2002-2012); Robert Rubin to Citigroup; Lawrence Summers as Treasury Secretary and later NEC director; Weill and Reed's lobbying, and Reed's later reversal.

- AI task-horizon trend: METR, time-horizon measurements, doubling roughly every seven months on the long trend and near four months recently; approximately 14.5 hours at the 50 percent horizon by February 2026; projected week-long tasks by late 2026 and month-long by mid-2027.

- Market concentration: the Magnificent Seven at roughly one-third of the S&P 500 in mid-2026, combined value above twenty-two trillion dollars, up from about an eighth of the index in 2015; Nvidia's rise since early 2023; AI-linked names driving the majority of 2025 index gains; Oxfam's early-2026 billionaire-wealth figure.

- Labor signals: 2025 outplacement data attributing tens of thousands of U.S. job cuts to AI within a total exceeding one million; a March 2026 workforce reduction from roughly ten thousand to under six thousand attributed to automation.

- Counterpoint acknowledged: Clinton, DeLong, and Cowen have argued the repeal did not cause, and may have softened, the 2008 crisis. The directional argument here does not rest on the narrow causation claim.